(888) 4-ALMEGA

[email protected]

About

Why?

Our Philosophy

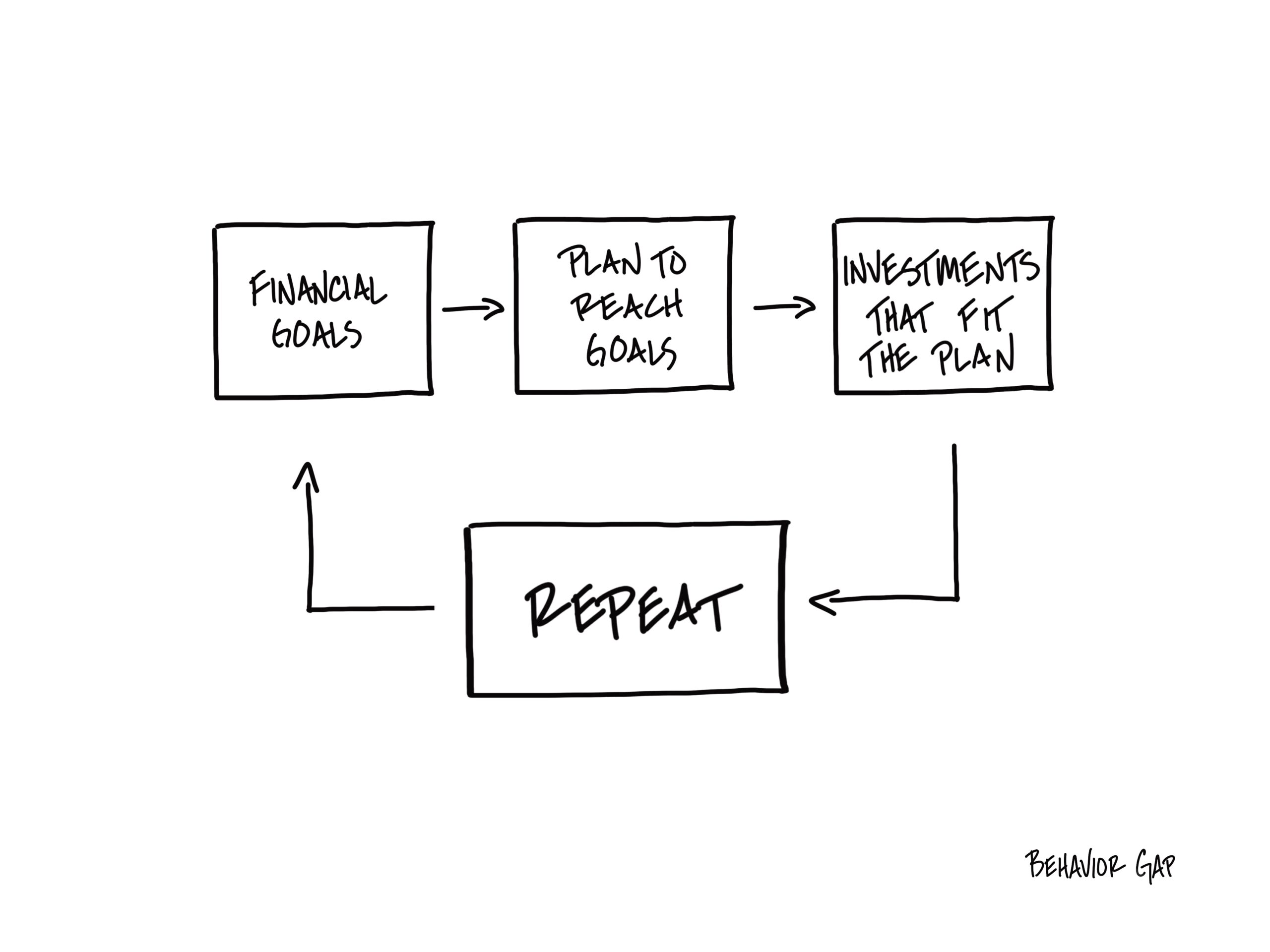

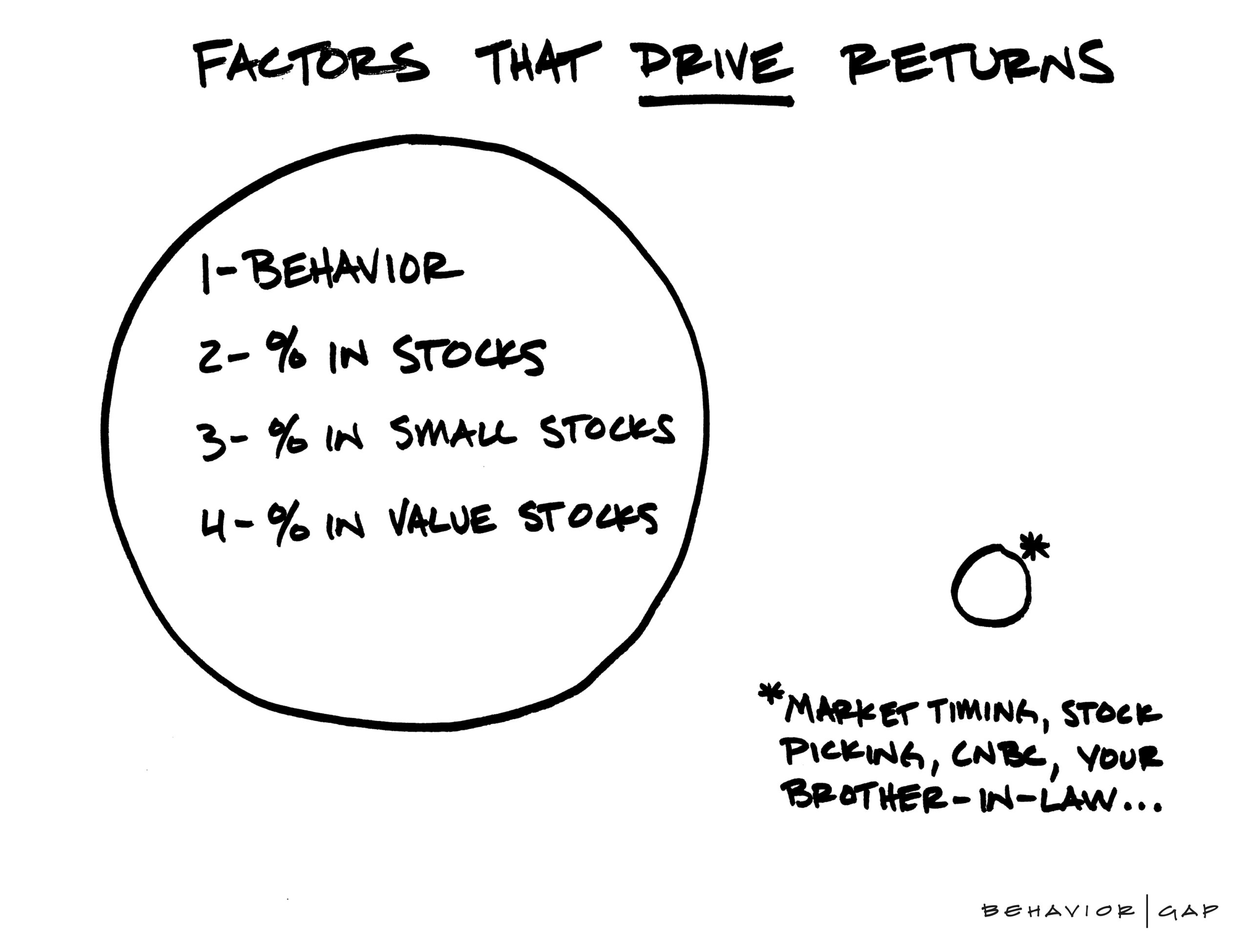

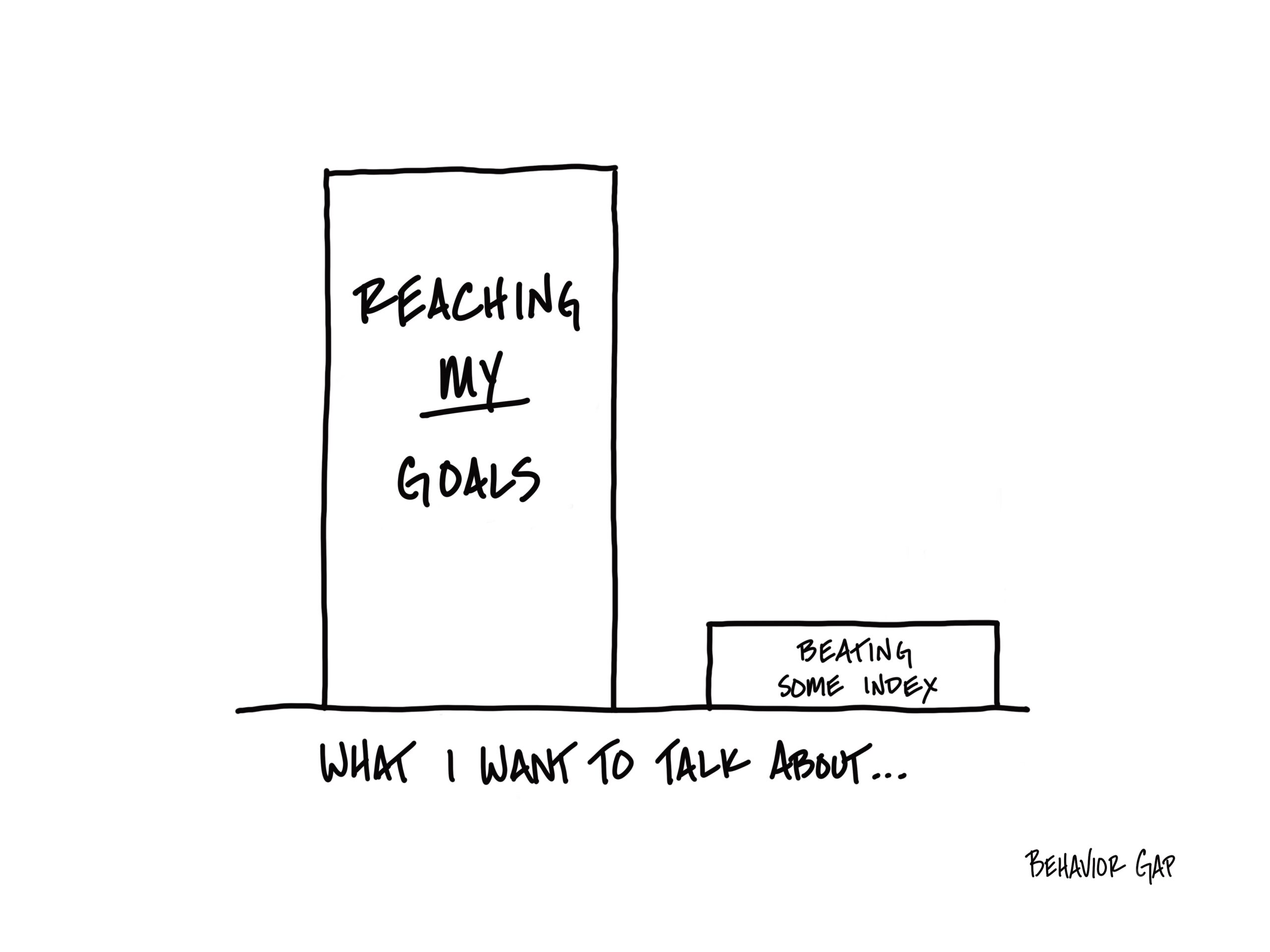

Our Formula

Our Process

Fee-Only Fiduciary

Our Custodians

Altruist

Charles Schwab

Zoe

Our Team

Services

Private Wealth Management

Ramsey SmartVestor

Investment Consulting

Passive

Custom

Cash Management

Performance

Core Portfolios

Core Wealth 20/80

Core Wealth 40/60

Core Wealth 60/40

Core Wealth 80/20

Core Plus Portfolios

Core Plus 40/60

Core Plus 60/40

Core Plus 100/0

Cash Management

Insights

Login

Client Portals

Client Reporting

Financial Planning

Launch™️

Estate Planning

Risk Quiz

Custodians

Charles Schwab

Altruist

Zoe

Mobile App Downloads

Contact

Select Page

To schedule a DISCOVERY MEETING call (888) 4-ALMEGA or click

GET STARTED